Young members are engaged in their health but also increasingly at risk: What medical scheme data tells us about youth health trends in 2025

South Africa's youth are taking charge of their health, while also dealing with evolving health risks. From proactively getting their health checks done to rising chronic disease trends, discover how young Discovery Health Medical Scheme members are engaging with their health and wellbeing, and shaping a healthier future for themselves.

Authors

Discovery's Health Intelligence members, Callan Kotzen (Actuarial Analyst), Chanie Suttner (Actuary), Matt Zylstra (Senior Principal Actuary), Amalia Theologides (Content Lead) and Lara Wayburne (Chief Health Intelligence Actuary)

Quick overview

South Africa's youth (defined as those aged 15 to 34) are often seen as healthy and at low risk of experiencing health conditions or serious healthcare concerns. Discovery Health Medical Scheme data tells a more nuanced story. Our analysis explores how young Scheme members are engaging with their health, what they're claiming for, and how their health risks are evolving. From rising rates of chronic conditions to unexpected high-cost hospital admissions, the data show that young members, while generally healthy, are not immune to health challenges. Among young members, mental health conditions have increased over time, with depression prevalence increasing more than thirteenfold since 2015. Meanwhile, multimorbidity is rising with chronic disease burden tripling since 2008. This analysis also highlights how youth claims are shifting, with psychosocial episodes now among the top four claim categories. There's also significant proof that young members are actively engaging in their health through Vitality Health Checks, maintaining their good health. This piece is a must-read for anyone interested in youth health trends, medical scheme dynamics, and the future of healthcare in South Africa. It's filled with data-driven insights, real-life examples, and clear implications for what is important in supporting young members to stay healthy - now and into the future.

Setting the scene: Reviewing the health and wellbeing of South Africa's youth population, and access to care

Young people's current health and wellbeing is a significant shaper of future healthcare demand and medical inflation.

South Africa's youth, which Statistics South Africa defines as people aged 15-34 years, form a crucial demographic, as they make up nearly one-third of the population. Between 2014 and 2024, the youth population grew by 2.3%, while the overall population increased by 13.9%.

Why are young, healthy members vital to any medical scheme's sustainability?

In South Africa, medical schemes operate as non-profit mutual funds. Member contributions are pooled to fund individual members' claims for relevant medical services and administrative expenses, with any surplus generated staying within the scheme.

In a community-rated medical scheme environment with open enrolment (guaranteed acceptance), young and healthy members facilitate age- and risk-related cross-subsidies within the risk pool.

- Community rated: All members pay the same level of premium contribution, irrespective of their current or historical health, or their age.

- Open enrolment: Members' age and existing health profiles may not disqualify them for medical cover in any approved medical scheme.

Ensuring a constant pipeline of young, healthy members joining a medical scheme is critical to the affordability of scheme membership (for all members) and to the scheme's long-term sustainability.

This is because younger, generally healthier lives claim less than they contribute. The surplus generated through young members is used to fund claims by older, generally sicker lives who are likely to claim more than they contribute to the pool. These young members will subsequently become beneficiaries of this cross-subsidy effect as they age or when they are sick, highlighting the principle of social solidarity on which medical schemes are based.

In the absence of this cross-subsidisation, schemes face an actuarial death spiral, requiring higher contributions each year from all members to compensate for the loss of the buffer that young, healthy lives represent. A situation like this is also compounded when, facing rising contributions and affordability pressures, healthier members may choose to avoid joining a scheme or withdraw from it until they feel they are getting value.

This fosters anti-selective behaviour, where a member joins a scheme anticipating a near-future claim, and erodes scheme affordability and sustainability.

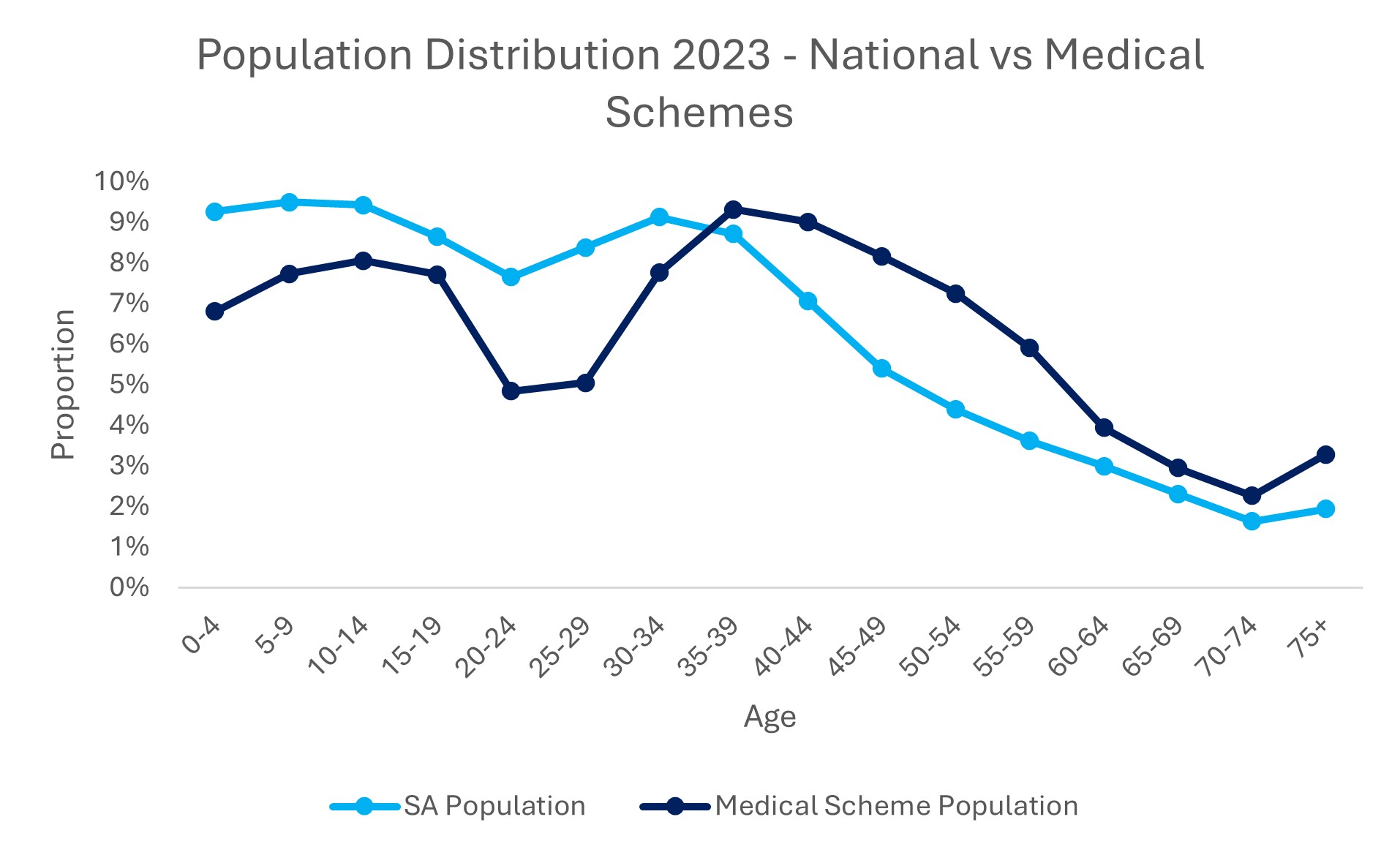

This phenomenon is evident in Figure 1, which shows the age distribution of the overall South African population, as well as the overall South African medical scheme population in 2023 (sourced from the General Household Survey 2023).

The light blue line shows how young people (aged 0 to late 20s) make up a significantly larger proportion of the overall South African population than of the South African medical scheme population, suggesting anti-selective behaviour - with young people mostly opting out of medical scheme coverage. There's a rise in medical scheme membership for people in their early 30s and particularly as people reach their early 40s - usually a time when healthcare utilisation is expected to increase.

Figure 1: Age distribution of overall South African population and South African medical scheme membership (Source: General Household Survey 2023).

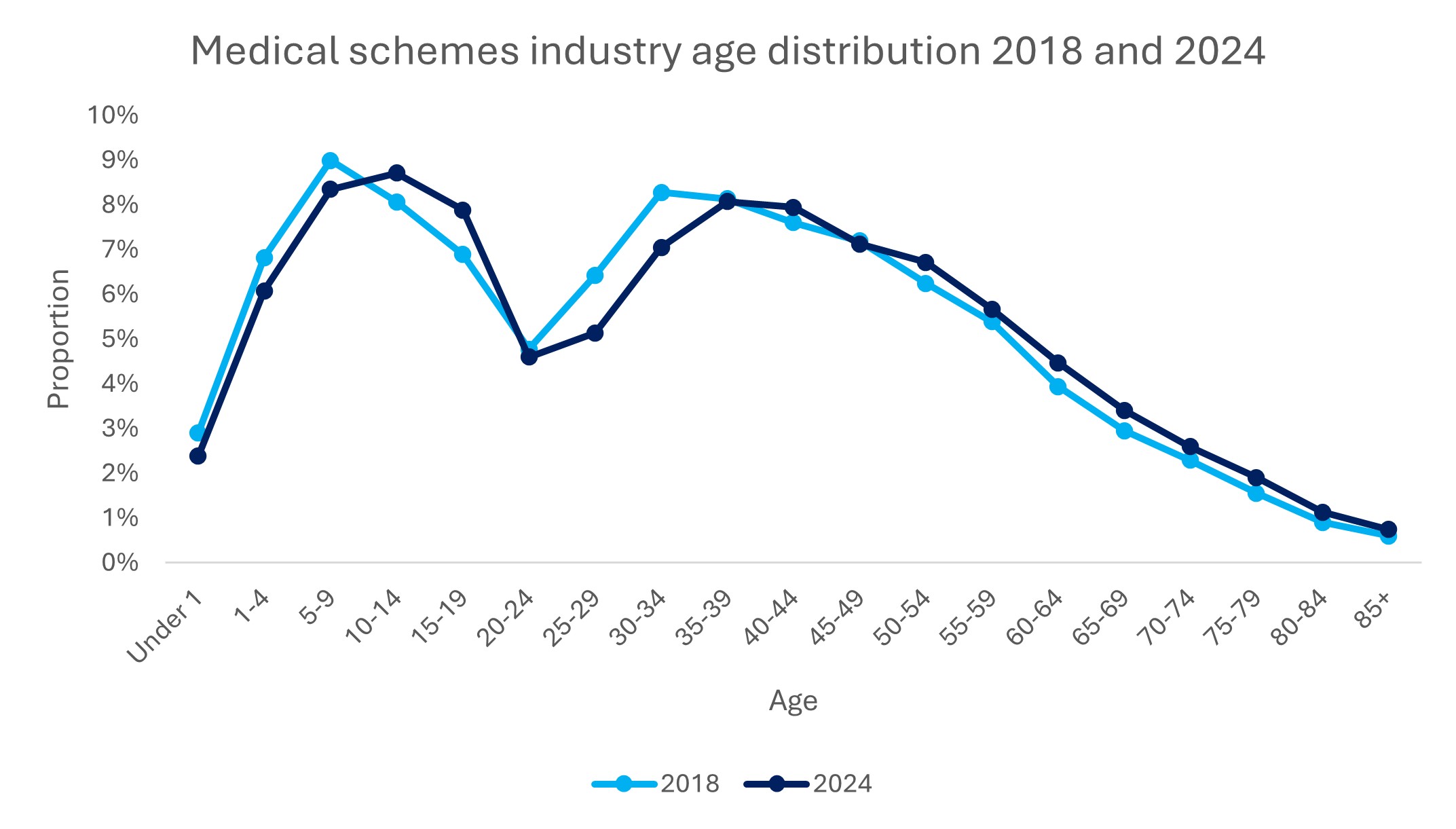

According to the Council for Medical Schemes, the number of young lives covered by medical schemes has decreased over the past decade. This trend, alongside chronological ageing, drives the overall ageing of the medical scheme population.

Figure 2 shows the age distribution of total medical scheme membership from 2018 to 2024 (data from Council for Medical Scheme Annual Report 2024).

In recent years, there has been a reduction in the number of babies added to the medical scheme as members. This drives the reduction seen in the proportion of child members over time. Children who were medical scheme members over a decade ago have retained their cover and become teenagers, for whom we see increased representation on medical schemes - the 2024 membership proportion is higher than in 2018 for ages 10 to 19, as shown in Figure 2.

Funding healthcare cover is often not a priority for young adults, so they tend to drop out of medical schemes as they start working, or when they reach the age at which they need to be removed from a parent's policy.

Figure 2: Age distribution of total medical scheme membership (Source: Council for Medical Schemes Annual Report 2024).

Joining a medical scheme early protects young members from unpredictable, high-cost health events

Joining a medical scheme early in life offers significant long-term benefits. Primary among these are avoiding the limited underwriting rules applied to late joiners and gaining long-term access to comprehensive coverage for a range of healthcare needs. For people of any age, one of the most important forms of cover offered through medical scheme membership is funding for unpredictable, high-cost events such as complex hospital admissions.

Naturally, young people may perceive themselves as at low risk of developing health conditions or complications. However, the reality is that life-changing events are unpredictable and can require high-cost hospital admissions that, without medical scheme cover, can be financially crippling when care is accessed in the private sector.

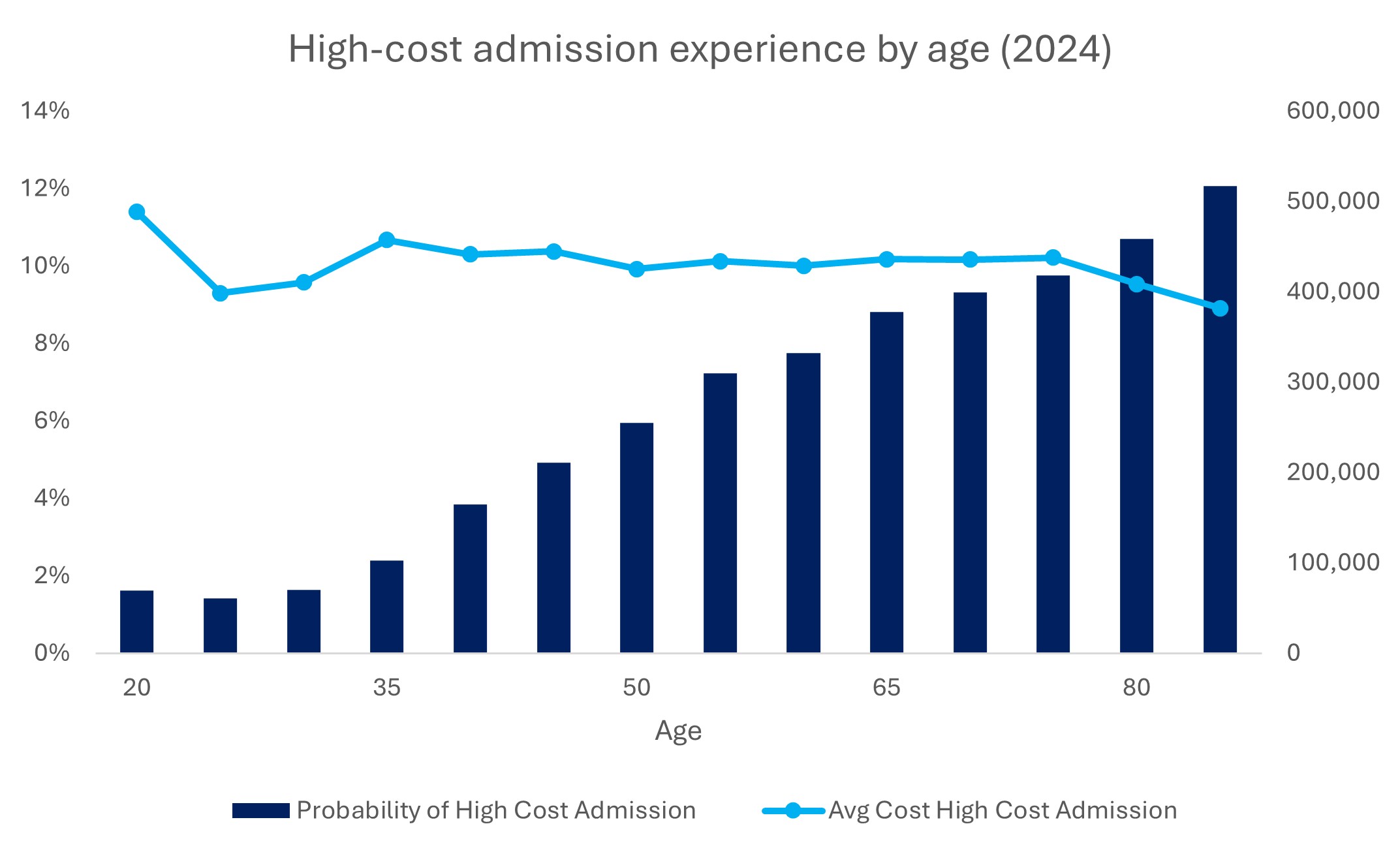

For the purposes of this analysis, we define a high-cost hospital admission as one resulting in claims to the Scheme of R200,000 or more.

Looking at Discovery Health Medical Scheme (DHMS) hospital admissions data for January to December 2024 (Figure 3) we see the proportion of high-cost admissions increasing with member age. However, the average cost of these admissions is for the most part independent of age (consistently around R400,000 per admission).

Figure 3: Probability of admission and average cost of high-cost hospital admissions (>R200 000) across age bands, for DHMS members (January to December 2024).

Three anonymised DHMS member stories showcase how high-cost events can impact young Scheme members. These anecdotes speak to the impact of high-cost admissions and health conditions alike:

- Trauma-related high-cost admission: A healthy member joined the Scheme aged 24 in July 2014. For the first nine years of the policy, this member experienced very low claims (R5 638 in total over nine years). At age 33, this member experienced an extreme, sudden trauma event, resulting in a hospital admission lasting 85.5 days. The member was on a ventilator for an extended period and, unfortunately, needed a subsequent high-cost admission straight after the first admission. This second admission was needed for an urgent procedure related to the initial trauma and required another 31.5 days in hospital. Overall, DHMS covered claims totalling R8.7 million for this member - an amount that most people accessing care in the private healthcare system would find financially crippling to self-fund.

- Cancer at age 17: A two-year-old DHMS member joined a DHMS Classic Priority benefit option in 2009. For the first 15 years of their membership, their healthcare claims were minimal, totalling just over R4 800. However, in February 2024, this member was diagnosed with leukaemia at the age of 17, requiring eight admissions to treat both the cancer and treatment-related complications. This member spent 147 days in hospital, with claims totalling R7.8 million in 2024.

- A gradual decline in a member's health due to serious chronic disease: This member joined DHMS at age 25 in January 2017 with no chronic conditions. Yet, they were diagnosed with type 2 diabetes mellitus shortly after joining the Scheme. Over the next few years, this young member was diagnosed with hypothyroidism, hypertension and hypercholesterolemia, and ultimately with chronic renal failure in September 2020. From this point on the member required dialysis, at a cost of R1.01 million a year, to be continued and covered for as long as they remain with the Scheme.

These stories make one thing clear. Even healthy young adults face unexpected health shocks - from trauma and cancer to the early onset of chronic diseases. When these events occur, the financial and emotional toll can be life-changing. Early medical scheme membership is not just about access to care; it's a vital safeguard against unpredictable, high-cost events that can alter a young person's future in an instant and significantly impact their loved ones too.

Young DHMS members are doing more Vitality Health Checks each year, and most members have four or five results in range

How is the way that young people engage in health-seeking behaviour shifting, and what do their claims patterns reveal? We investigate this through the lens of engagement in Vitality Health Checks.

- The Vitality Health Check is a screening test carried out at an accredited Vitality Wellness Network provider (Pharmacy, General Practitioner, Discovery Store or at a Discovery Wellness Day).

- The Vitality Health Check screens for health risks across five key measures: waist-adjusted body mass index, blood pressure, blood glucose, cholesterol, and smoking status.

- This simple, convenient and accessible set of essential health screenings provides an annual (or more frequent) benchmark a member's risk of lifestyle-related chronic illnesses, either to prevent the onset of disease or identify possible health concerns as early on as possible.

The Vitality Health Check is available to adult Vitality members. Many DHMS members are also Vitality members. However, during 2023 and 2024, Vitality Health Checks were made available to all members of DHMS (including those who are not Vitality members), as completing a Health Check unlocked access to the WELLTH Fund.

The WELLTH Fund was a once-in-a-lifetime benefit through which members could earn up to R10, 000 per family to spend on a wide range of important healthcare services (designed to encourage members to seek out proactive care). The broader idea was to overturn the decline in preventive screening rates caused by the COVID-19 pandemic.

The WELLTH Fund's design therefore promoted the uptake of Vitality Health Checks in 2023 and 2024 and this is evident among young DHMS members.

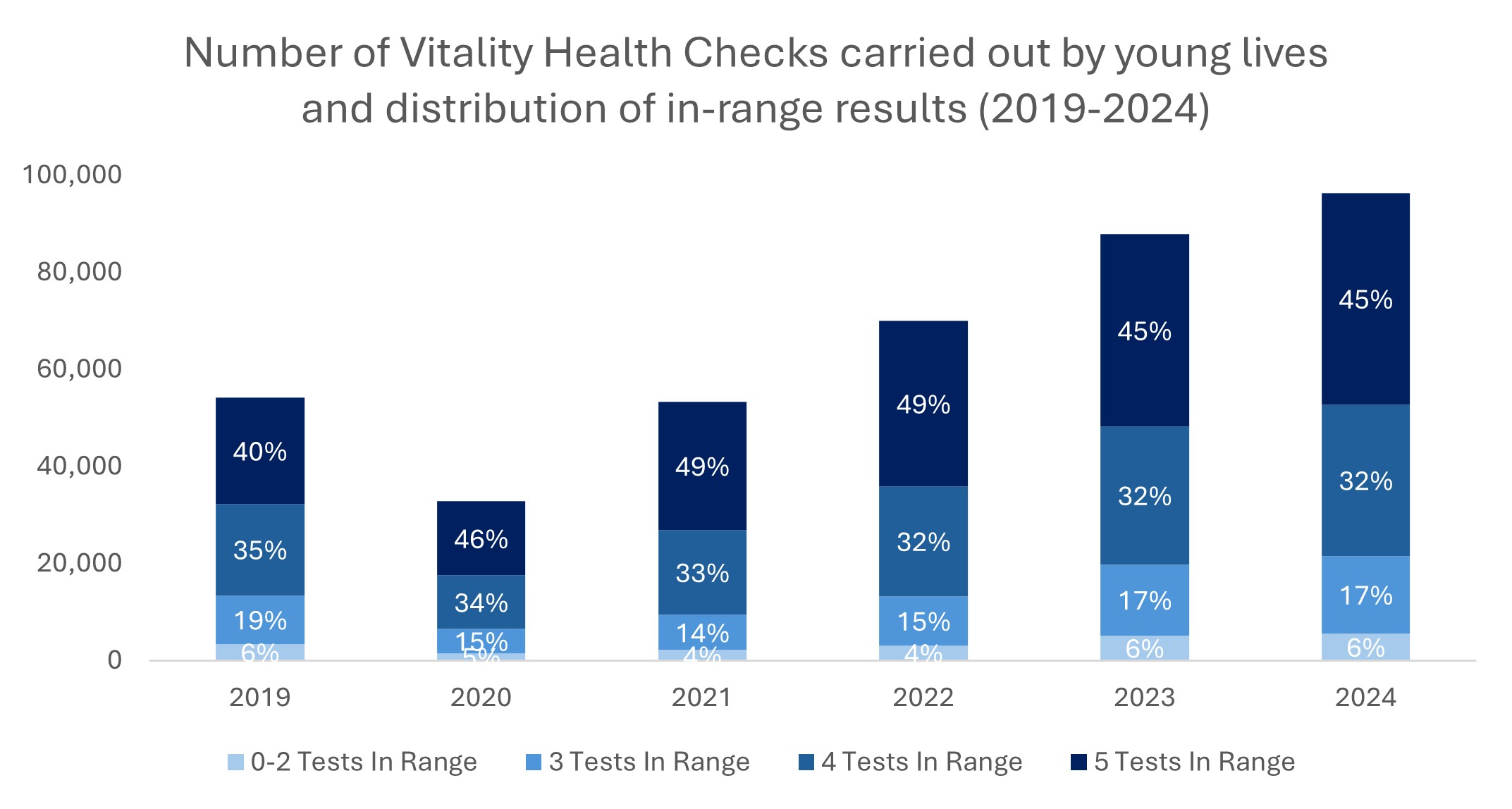

Figure 4 shows the number of Vitality Health Checks carried out by young DHMS members from 2019 to 2024 (the uptick in 2023 and 2024 is evident). The graph shows pre-pandemic levels and the dip in 2020, the first year of the COVID-19 pandemic. The proportion of in-range results are also indicated over time.

What we see here is that young Scheme members are increasingly engaged in health-promoting behaviour (which is what doing a Vitality Health Check is all about). We also see a consistency in the number of in-range results, with four or five in-range results predominant over time.

Considering the CMS data mentioned above, these trends are important as they show that young people joining DHMS are both healthy and interested in maintaining their good health.

Figure 4: Vitality Health Checks carried out by young DHMS members from 2019 to 2024 with the proportion of in-range results (from zero to five test result options) indicated for each year.

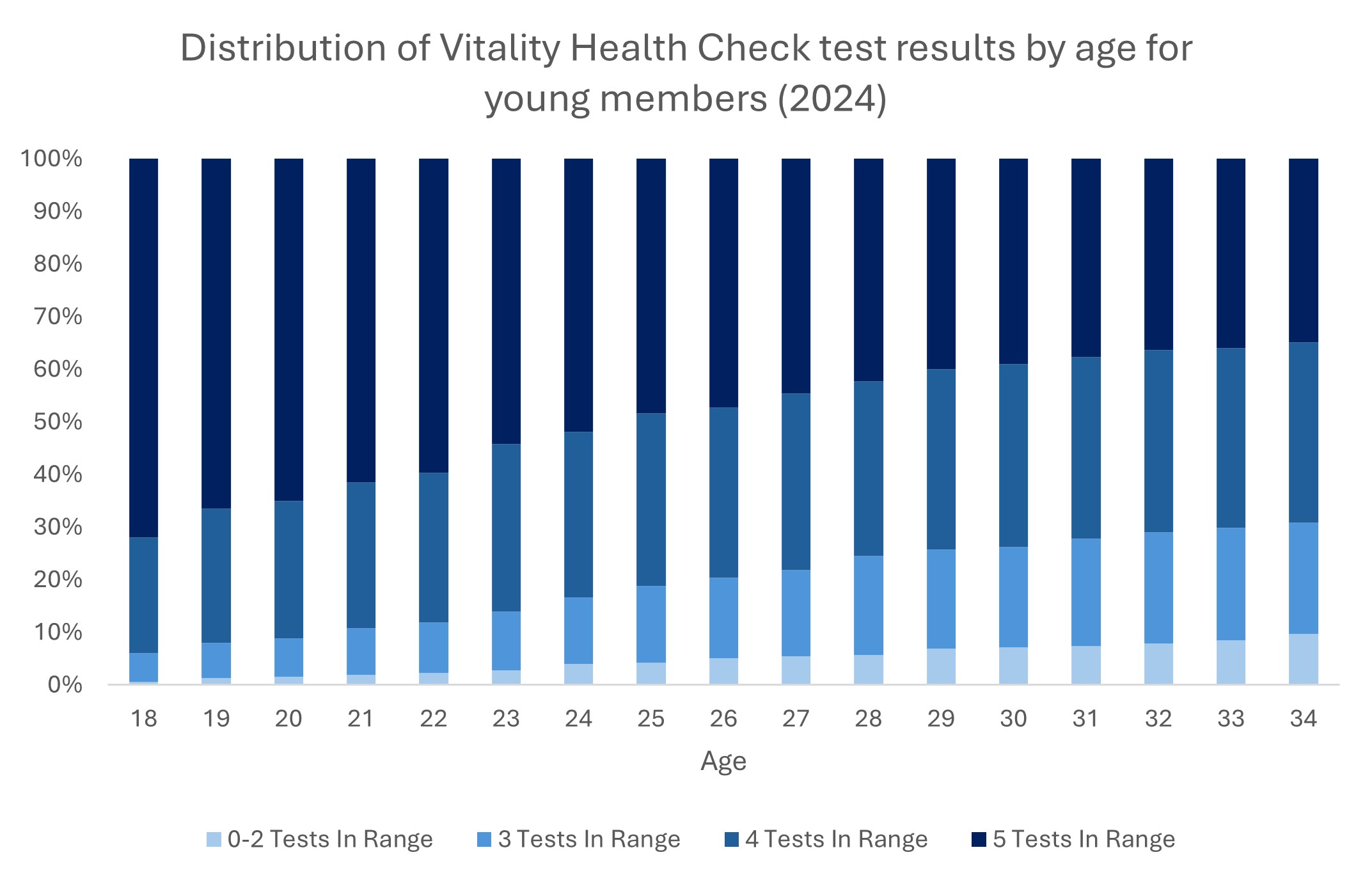

Figure 5 illustrates the decline in the proportion of in-range Vitality Health Check results as members age. In 2024:

- 72% of 18-year-old members had all 5 results within range, with 0.2% of this group showing two or less results in range.

- By age 34, only 35% of members had all 5 results in range, and 10% had two or less results in-range.

These findings highlight the importance of regular health checks for young people as means through which to detect the early onset of the risk factors for chronic non-communicable conditions or to manage any diagnosed health conditions optimally.

Figure 5: The number of in-range Vitality Health Check results in young Scheme members by age (across ages 18 to 34) in 2024, showing that most young people have four or five results in range.

How healthy are young Discovery Health Medical Scheme members?

Young people are generally healthier than older people, and this trend is evident within the DHMS member base (discussed in the section above, which examined in-range Vitality Health Check results).

However, our in-depth analysis of the health status of young members reveals an increase in chronic conditions among them over time.

18% of young members were registered for a chronic condition in 2024

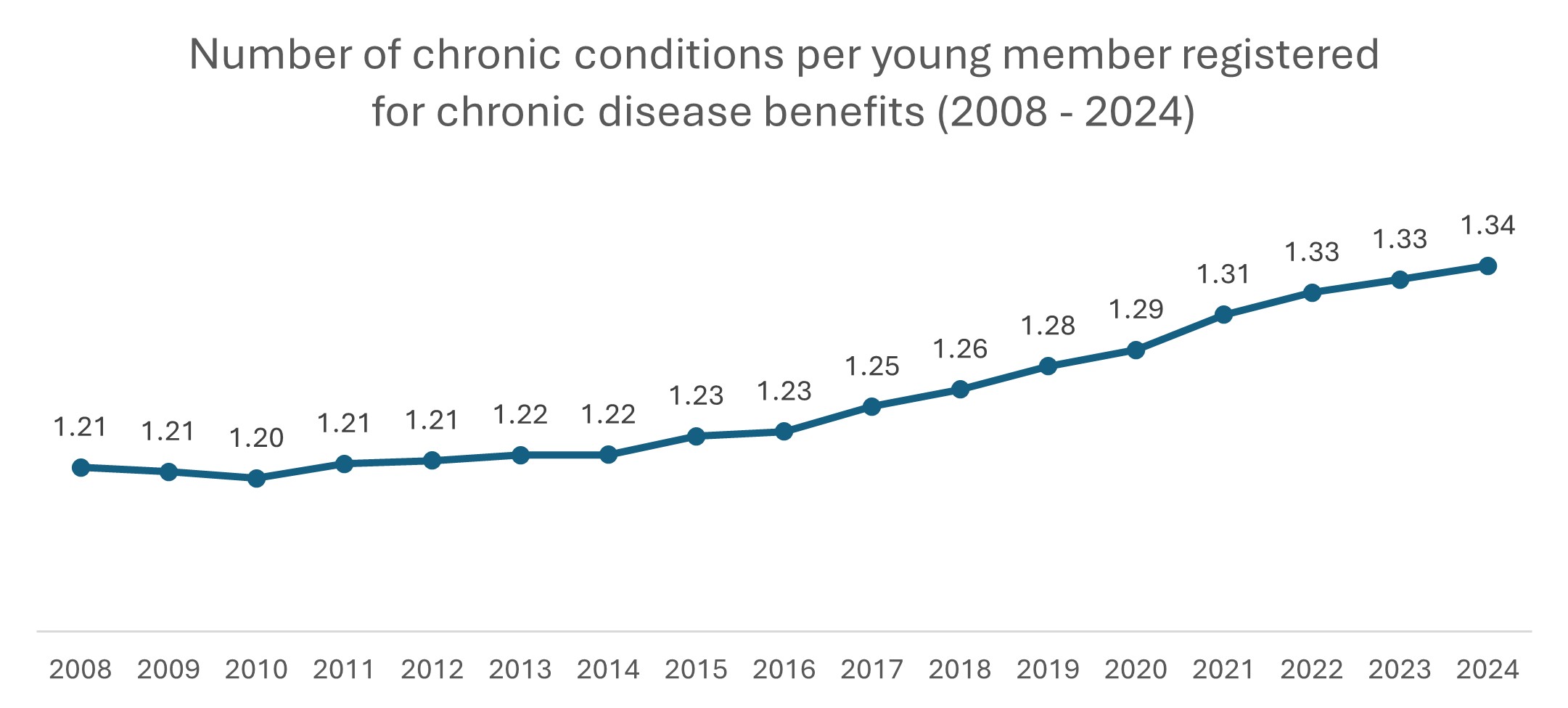

In August 2024, almost one-fifth, or 18%, of DHMS young members were registered for one or more chronic conditions, a tripling from 6% in 2008 (measured by registration for the Chronic Disease List as part of the Prescribed Minimum Benefits for the Chronic Illness Benefit).

The average number of chronic conditions per young member aged from 15 to 34 is also increasing, from an average of 1.21 in August 2008 to 1.34 in August 2024. This indicates the accelerated rise in multimorbidity among young people over time.

Figure 6: Average number of registered chronic conditions per chronic young member over the period 2008-2024.

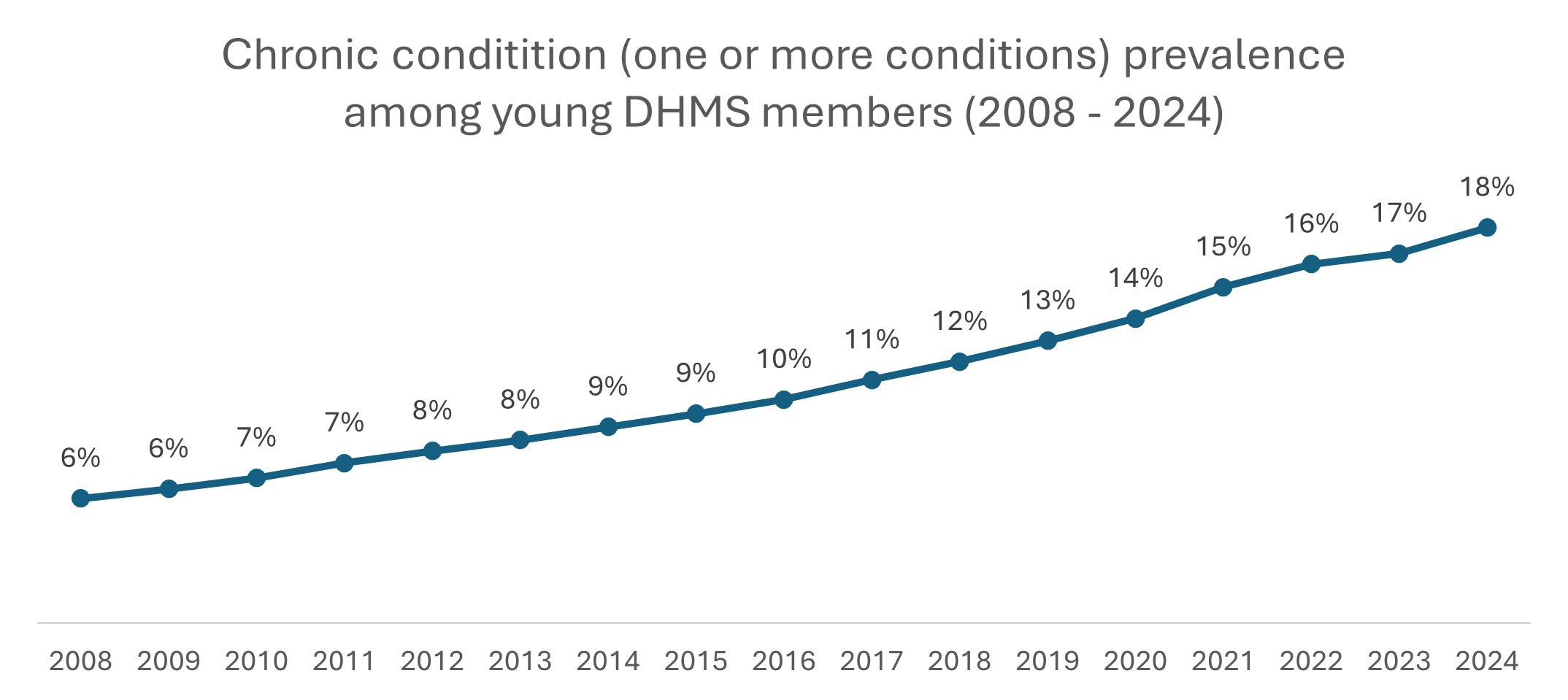

Figure 7 shows the proportion of young DHMS members registered as living with at least one chronic condition (so, one or more conditions) over the period 2008-2024. Where the prevalence of young members living with one or more conditions was relatively stable from 2008 to 2016 (from 6% to 10%), there has been an accelerated rise in chronicity from 2017 to 2024 (from 11% to 18%).

Figure 7: Proportion of DHMS young lives registered with at least one chronic condition over the period 2008-2024.

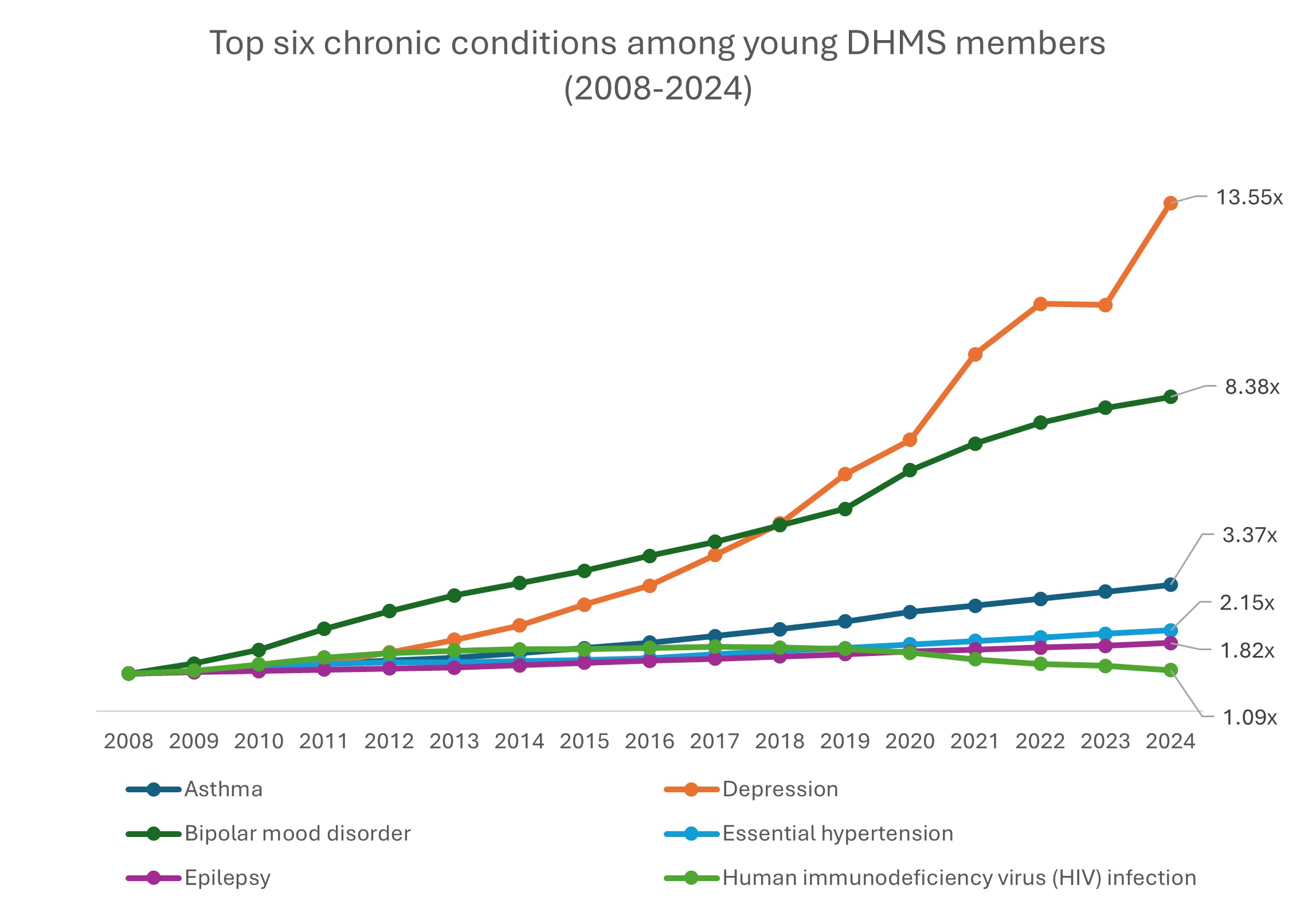

Depression is the biggest contributor to the overall increase in the chronic prevalence for young members. Figure 8 illustrates the rise in prevalence from 0.4% in August 2015 to 5.9% in August 2024, representing a 13.55-fold increase.

There's also been an increase in the prevalence of bipolar mood disorder - from 0.4% in 2008 to 3.5% in 2024 - an 8.38-fold increase.

- These dynamics are not unique to young Scheme members. Read a summary of our recent three-part analysis on mental health condition prevalence across the Scheme population to find out more, or visit part 1, part 2 and part 3.

Thereafter, the next most prevalent conditions in young scheme members are asthma (3.37-fold increase in prevalence), essential hypertension (2.15-fold increase in prevalence) and epilepsy (1.82-fold increase in prevalence), and HIV (for which we see a reduction in prevalence specifically from 2017 onwards).

These trends highlight two important themes:

- The selective purchasing and retention of medical scheme cover or the tendency for healthier young adults to opt out of medical scheme cover, while those with existing health needs are more likely to join or remain on the Scheme.

- The extent to which young DHMS members are impacted by mental health and non-communicable diseases such as hypertension - a risk factor for heart disease, stroke, kidney damage, vision loss and more.

Figure 8: Chronic condition prevalence (2008-2024) for the six conditions most prevalent among young members in August 2024 (indexed to August 2008, i.e. values in the graph are multiples of that condition's prevalence in August 2008).

What sort of care are young members claiming for?

Going deeper into young members' healthcare claims helps us better understand their healthcare needs.

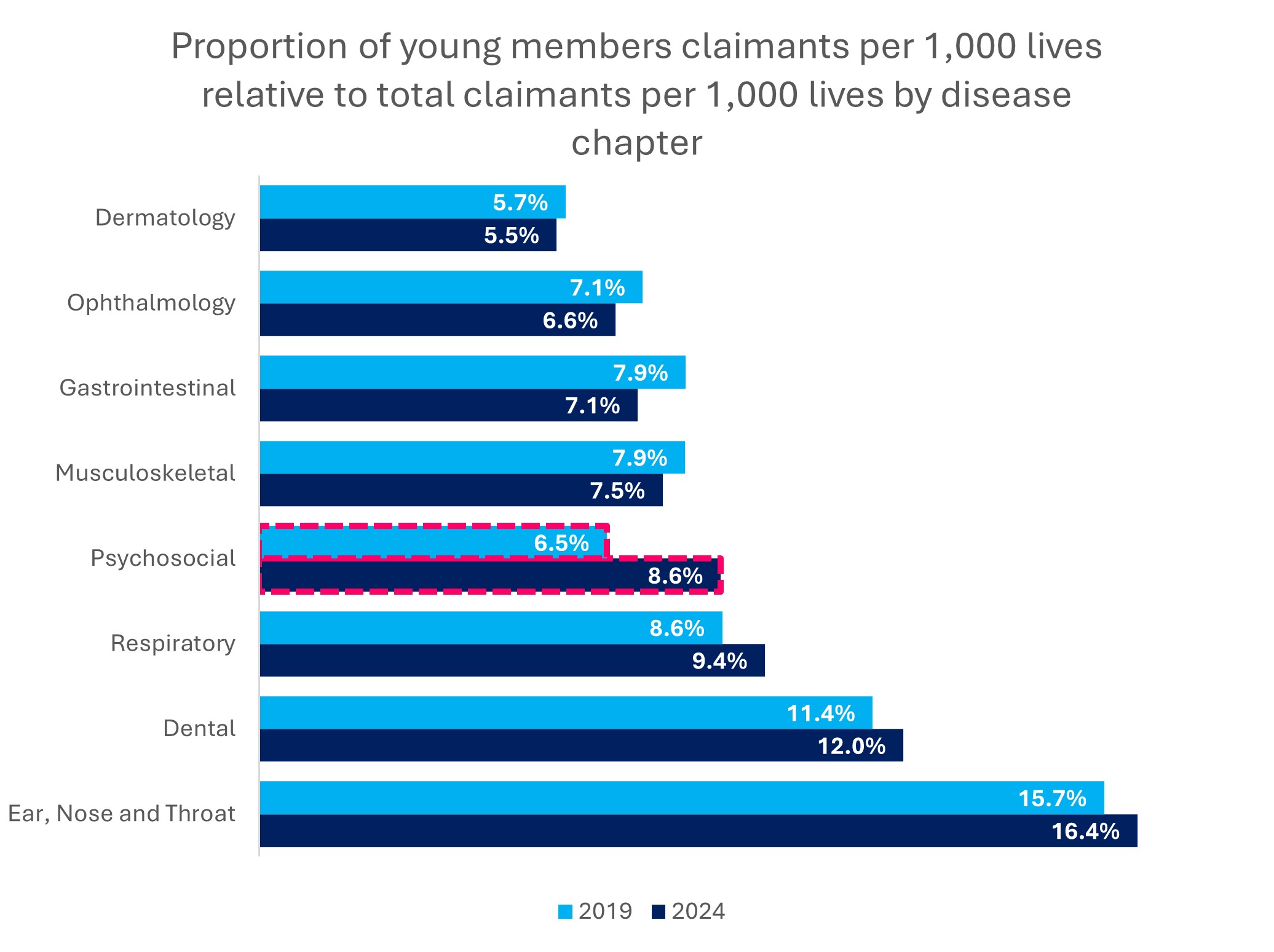

Claims are analysed by disease episode (which reflects the clinical classification of the care rendered). In 2024, young members claimed most often for Ear, Nose and Throat care (16.4% of all claims), followed by dental, respiratory and psychosocial (mental health) care.

The psychosocial disease chapter is of particular interest. The proportion of young member claims for this disease chapter has increased from 6.5% in 2019 to 8.6% in 2024, and from 2019 to 2024, the number of claims has increased 3.8% per annum. This is in line with the rise in prevalence of depression and bipolar mood disorder in young Scheme members discussed earlier.

Figure 9: Proportion of claims by young members relative to total claims, across the top disease chapters claimed for by young members, and comparing 2019 to 2024.

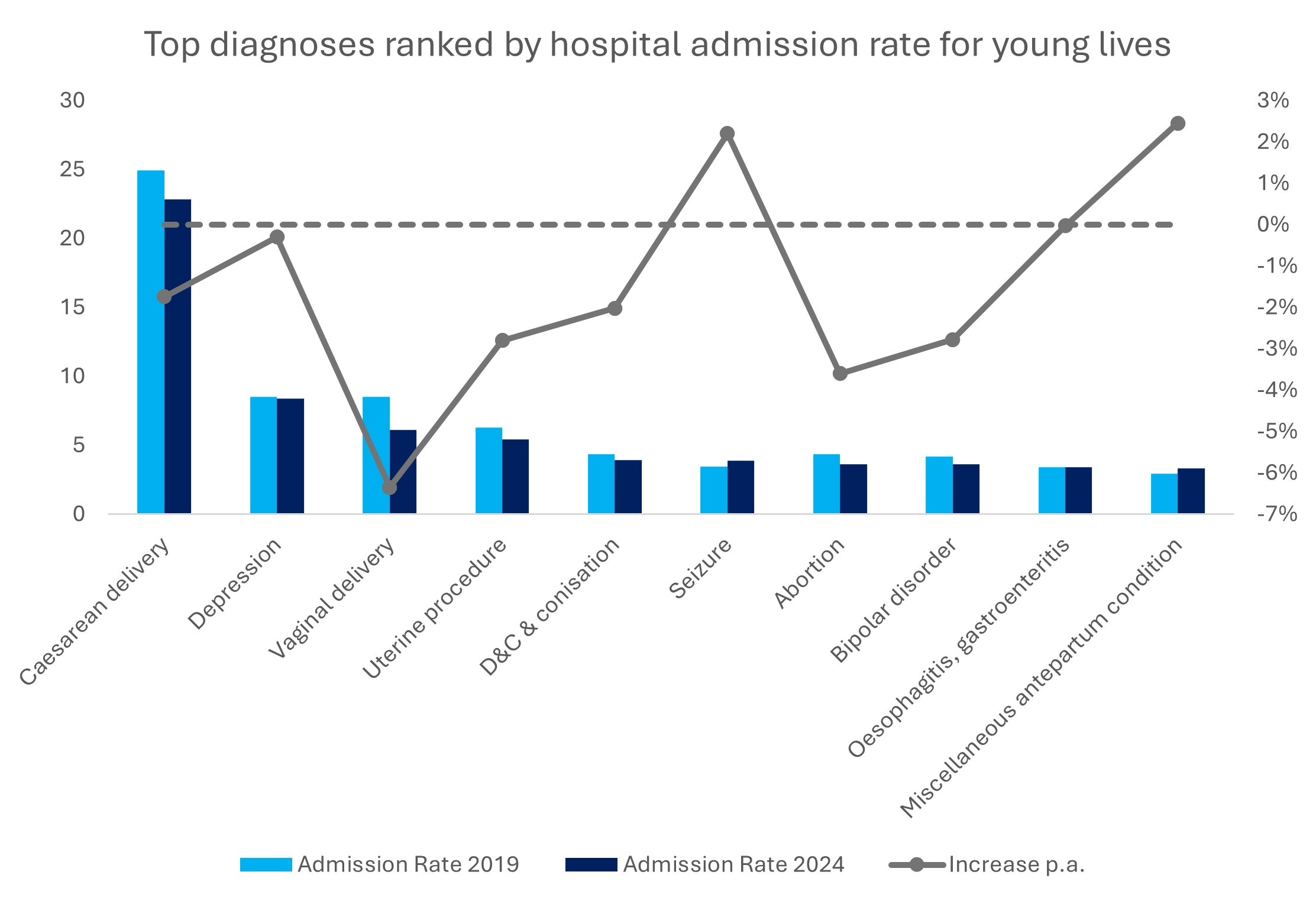

Figure 10 shows rates of admission to hospital for young members, comparing 2019 to 2024 across a range of reasons for in-hospital care:

- Giving birth via caesarean section has consistently been the most common reason for admission to hospital over time, with a slight decrease in this rate from 2019 to 2024.

- The second-highest rate of admission is seen for depression-related in-hospital care (with very similar rates from 2019 to 2024), followed by admissions for vaginal delivery.

- Vaginal deliveries have experienced a significant 6.4% decline in admission rate over time.

- This reduction, coupled with the decline in the admission rate for caesarean sections, indicates a general decrease in birth rates among the young population over time.

- There have been decreases across eight of the top 10 reasons for admission for young lives from 2019 to 2024.

- The two remaining areas are an exception:

- Seizures experienced a 2.2% increase in admission rate - influenced by rising prevalence of neurological disorders such as epilepsy and accompanying mental health conditions amongst young lives.

- Miscellaneous antepartum conditions are the other exception, showing a 2.5% increase in admission rates. These conditions pertain to more complex pregnancies, which can be linked to increased chronic condition prevalence among young Scheme members.

Figure 10: Top diagnoses ranked by hospital admission rate for young lives - comparing 2019 admission rates to rates in 2024.

Conclusion

This analysis reveals important information about the healthcare areas that are most relevant to young DHMS members. Let's review the DHMS young member health trends we've covered in this article:

- Youth engagement in health checks is rising: Young members are increasingly proactive about their health, with more Vitality Health Checks completed each year (particularly in 2023 and 2024 driven by access to the WELLTH Fund benefit) with most members achieving four or five (out of five) results in range, and the proportion of four or five results in range dropping off as young people age. This emphasises the importance of monitoring one's health status at a young age and maintaining positive health habits throughout young adulthood and into older age.

- Chronic conditions are on the rise: The proportion of young members registered for at least one chronic condition has tripled since 2008, reaching 18% (almost one-fifth of the young member base) in 2024, with essential hypertension being a leading contributor.

- Mental health needs are growing: Depression prevalence among young members has increased more than thirteenfold since 2008, and bipolar mood disorder is also rising sharply.

- Claims patterns are shifting: Psychosocial (mental health) episodes are now among the top four claim categories for youth, reflecting changing health needs. Most young members claim for ear, nose, and throat-related care, followed by dental and respiratory care. Psychosocial episodes (the fourth highest category) have experienced the largest increase in claims over time.

- High-cost health events can affect anyone: Even healthy young adults have experienced unpredictable, high-cost healthcare events, highlighting the value of joining a scheme as early as possible in one's life. While admission rates are lower for youth than older members, the cost of complex admissions is similar across age groups. Medical scheme cover provides comprehensive benefits in the event of an emergency or high-cost hospitalisation, and this cover proves to be valuable irrespective of age.

The youth are a critical segment of the medical scheme risk pool in South Africa. Young scheme members contribute to the growth and sustainability of medical schemes; they promote affordability and strengthen the Scheme's ability to pay claims for all members through cross-subsidisation between cohorts of members. As mentioned in our introduction, reporting by the Council for Medical Schemes indicates that the number of young lives covered by medical schemes decreased over the decade from 2018 to 2024. This trend, alongside chronological ageing, drives the ageing of the medical scheme population. This is why it's critical that Schemes attract young and healthy lives and, once onboard, support them to remain as healthy as possible for as long as possible.

Expanding awareness and accessibility of these medical scheme opportunities is essential for empowering South African youth to take charge of their health and well-being.

How is Discovery Health Medical Scheme ensuring a growing relevance for South Africa's young people?

As mentioned in a recent media release Discovery Health Medical Scheme continues to prioritise affordability and access for younger members through a series of deliberate, future-focused initiatives and plan options.

In September 2025, the Scheme announced that it would defer its 2026 contribution increases to 1 April 2026 across all plan options and for all Scheme members, delivering an estimated R1.5 billion in direct savings to members (from January to end March 2026). This deferral means contributions remain at 2025 levels for the first quarter of 2026.

Importantly, the Active Smart plan will have a 0% contribution increase for 2026, underscoring DHMS's commitment to affordability for young professionals. Since its launch in January 2025, Active Smart has grown to more than 22 000 lives, with over 80% of new members under 40, making it the fastest-growing new plan in the Scheme's history.

Building on this success, DHMS will also launch the Smart Saver Series on 1 January 2026, designed around the healthcare and financial needs of young, growing families. The new Classic Smart Saver and Essential Smart Saver plans combine comprehensive hospital cover with guaranteed day-to-day benefits for the healthcare services families use most - including GP consultations, dentistry, optometry, prescribed and over-the-counter medicine, and contraceptives - as well as maternity, mental health and oncology benefits within the Smart Network. By integrating a Medical Savings Account with the Personal Health Fund, Smart Saver provides both certainty and flexibility in the way in which members fund their day-to-day healthcare.

Together, these initiatives reflect a coherent strategy to attract and retain younger, healthier lives in the Scheme. Through the Active Smart plan, the Smart Saver Series, and enhancements to the Personal Health Fund and Personal Health Pathways, DHMS is meeting the evolving needs of young South Africans who want affordable, flexible access to private healthcare. This reinforces the Scheme's leadership in building a sustainable, prevention-focused medical scheme that supports members' wellbeing at every life stage.

- Stats SA definition of Young Lives https://www.statssa.gov.za/?p=18083

- General Household Survey 2023 https://isibaloweb.statssa.gov.za/pages/surveys/pss/ghs/2023/ghs2023.php

- CMS Annual Report 2024 https://www.medicalschemes.co.za/publications/#2009-3817-wpfd-industry-report-2024-1764849328

Interested in knowing more or reporting on these findings?

Please contact us on MEDIA_RELATIONS_TEAM@discovery.co.za to request any updated data available since publication and to obtain any further context required.

Did you find this post interesting?

Please visit our Discovery Health Insights Hub for a range of analyses and insights shared by our Discovery Health Intelligence Team over time, covering various health-related themes.

All information shared on this page is based on perspectives gained from analysing data acquired by Discovery Ltd and its various affiliate entities (Discovery). The analysis, which is conducted by Discovery's actuarial and data science team, aims to encourage industry dialogue. Publications containing our analyses are shared for educational and informational purposes only. Each publication reflects only these data available for analysis at the time of publication. It does not, unless otherwise indicated, constitute peer-reviewed, published scientific research, and hence should not be interpreted as such or used as a basis for altering treatment decisions. While every effort has been made to ensure the accuracy of the content conveyed, we cannot be held liable or responsible for any actions or decisions taken based on the information shared in this article.